Institutional Performance Management

Move forward with precision

Drive enrollment & retention, manage expenses, and improve learning outcomes. HelioCampus helps you navigate today's high stakes with best-in-class Data Analytics, Financial Intelligence tools, and a robust Assessment & Credentialing platform.

Trusted By

.png)

Data Analytics

Empower campus leaders to ensure student success, accelerate decision-making, and optimize operational processes with a secure data platform that helps you uncover actionable insights from across the student lifecycle. Plus the HelioCampus secret sauce - our data science and analytics services - help you and your team build data fluency, drive change, and advance analytics priorities on your campus.

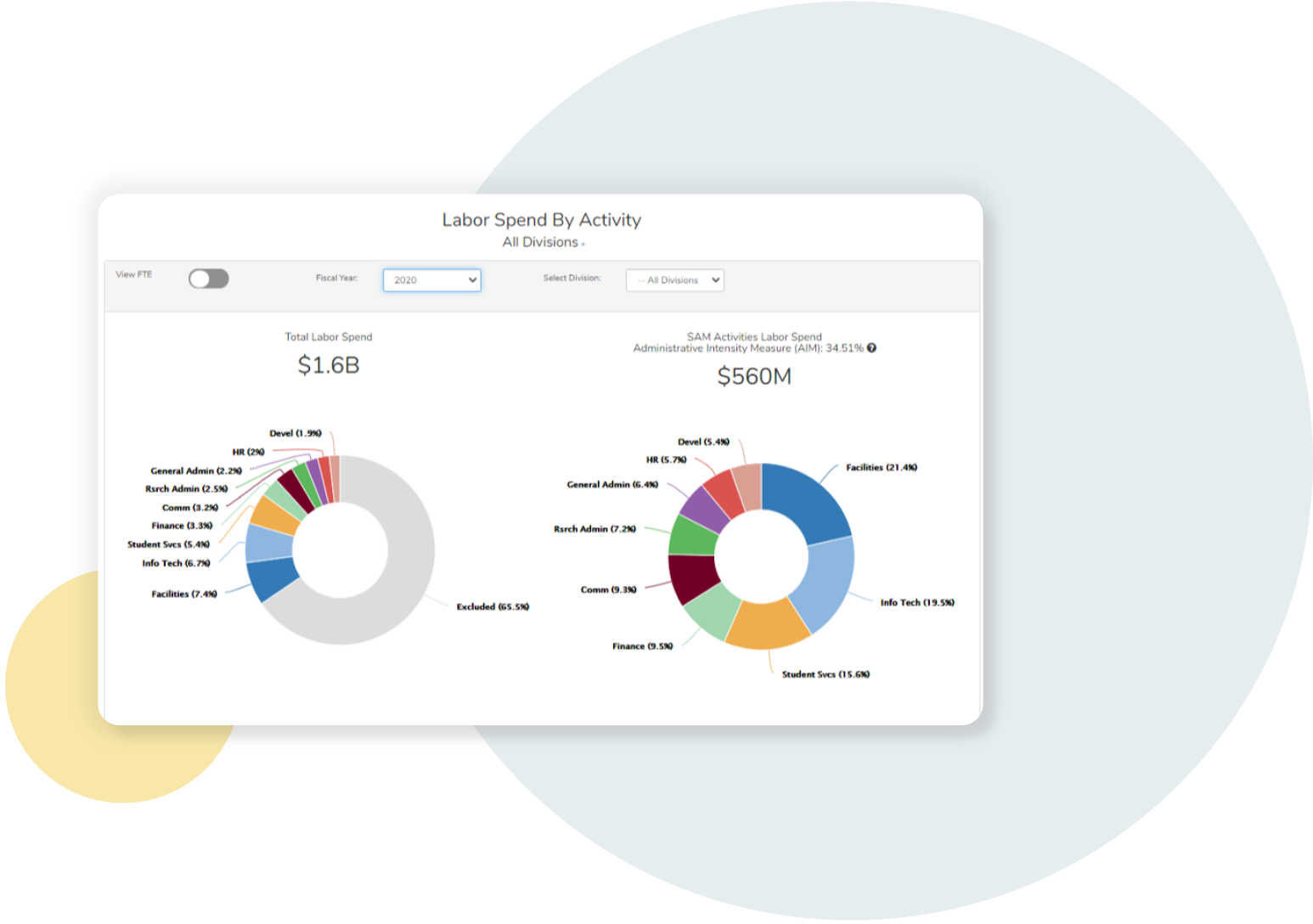

Financial Intelligence

Get deep financial insights to power essential administrative operations like annual budgeting, workforce planning, and financial sustainability efforts. Only HelioCampus offers higher ed business and operations leaders access to benchmarked labor data, long range financial projections, and a finance community of practice to help you plan for a variety of scenarios, understand costs, mitigate risks, and chart a path to their mission.

Explore Financial Intelligence

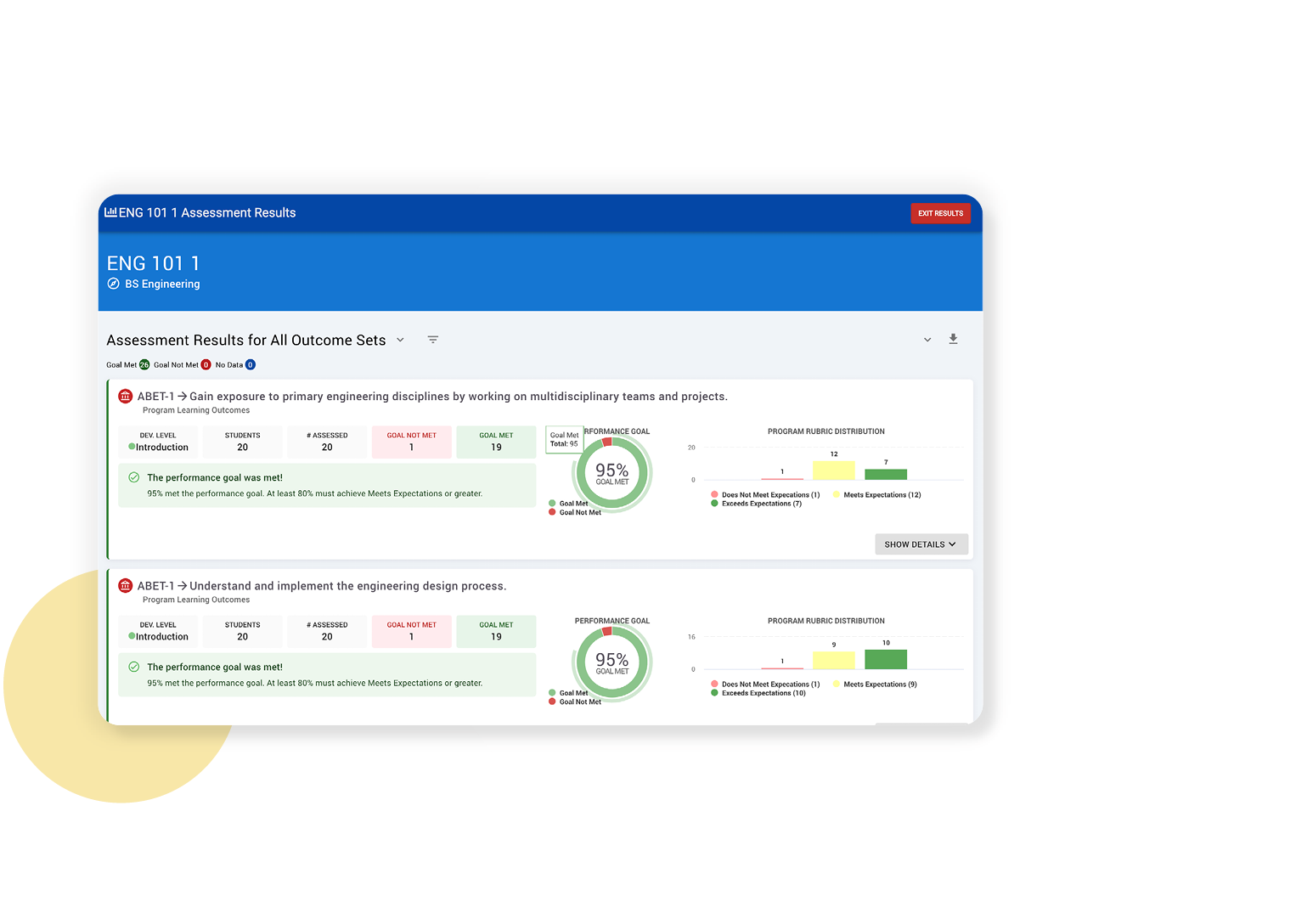

Assessment and Credentialing

Assess student learning outcomes in real-time with a unified platform that empowers you to seamlessly access assessment data and leverage it for accreditation, planning, and continuous improvement. Our technology gives stakeholders - from students to faculty and administrators - fast access to the data and evidence they need across courses, programs, and outcomes.

Explore Assessment and Credentialing

scale.

Making an impact with our clients

Working in higher education today requires leaders to navigate growing pressures in new ways. Hear how our clients and leadership team are thinking about this critical moment through the lens of Institutional Performance Management.

Powering insights for higher education at forward-thinking institutions